Your business is about to begin in the US. Your team is strong and you have an excellent idea. Your business plan is well-thought out. Before you start, decide which type of entity is best for your company.

The type of entity you select will determine how your business’s taxation and regulation is handled. The key factors that determine your choice of business entity are:

-

Taxation of profits

-

Complexity and costs of setting up a business as well as governance and administrative issues

-

Protection of personal assets from liability, especially for owners

In some instances, the decision is obvious. But it’s not always. The legal and tax implications of each entity are unique, so deciding which is best for your business can be difficult.

With more than 20 years of experience in accounting–including more than 14 years of providing CFO services to companies across multiple industries–I have advised numerous C corporations, S corporations, LLCs, and partnerships on tax and entity-choice matters. This article will present you with the most important points that need to be considered when making this choice.

Please note that this is only a general guide. Certain details might not be applicable to your business. Tax or legal advice should be sought before making any final decisions.

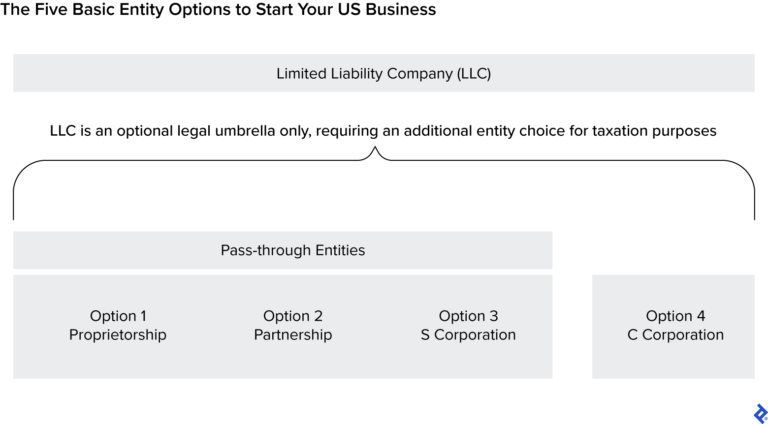

Understand the different types of business entities

IRS recognizes 4 main business entity types: partnership, proprietorship, C corporation and S corporation. The IRS recognizes four main types of business entities: proprietorship, partnership, S corporation, and C corporation.

It’s crucial to first understand the pass-through entity before we discuss business entities or LLCs.

What are Pass-through Entities (PTEs)?

All pass-through entities are proprietorships, partnership, and S corporations. The reason they are known as pass-through entities is because the taxable income of these businesses “passes” through to their owners’ personal tax returns and gets taxed in those tax returns.

S-corporations and partnerships file tax returns for their companies, but they only display the taxable income of the business and distribute that income among the owners using a Schedule K-1. The Schedule K-1 amounts are then taxed and reported on each owner’s personal tax returns (Forms 1040) as well as any applicable state or local tax returns.

Contrary to this, sole proprietorships do not file any business tax returns. Business income is directly calculated on the Schedule C, Schedule E or Schedule F in Form 1040.

The pass-through status has a lot of significance because owners who are a part of such entitites pay their personal income taxes on company profits, and then they receive tax-free distributions of those profits from the entity. It is different for C corporations who not only pay income taxes but hold dividends that are taxable. The C corporation is liable to pay tax first on the income it earns. Any remaining funds are then distributed to stockholders who must also pay income taxes. Double taxation is what this situation amounts to.

|

|

||

|---|---|---|

|

|

|

|

|

Income Taxable |

$1,000,000 |

$1,000,000 |

|

Tax rate on corporate income |

N/A |

21.0% |

|

Individual tax rates |

37.0% |

N/A |

|

Corporations owe tax |

$0 |

$210,000 |

|

Owners owe tax |

$370,000 |

$0 |

|

Cash after tax |

$630,000 |

$790,000 |

|

Rate of tax on the distributions to owners |

0.0% |

23.8% |

|

Dividend distributions are subject to additional tax |

$0 |

$188,020 |

|

Net after-tax cash remaining |

$630,000 |

$601,980 |

The C Corporation’s double taxation issue is lessened by the other advantages of this type of entity, including the lower tax rate for corporate profits, and the unlimited allowance to shareholders. The cons of C corporations will outweigh their pros for most small and midsized businesses.

Let’s examine the differences between S corporations and C Corporations in more detail now that you’ve made this key distinction.

What are sole proprietorships?

In essence, sole proprietorships refer to simple businesses that are owned by a single person or married couple. These businesses include freelancers, consultants, small businesses that provide services, food stands and so on. Solle proprietorships do not have ownership shares, so the only way to exit is by selling the assets.

The simplest type of business is a sole proprietorship. By default, any business which starts up without formal incorporation is a sole ownership (depending on how many owners there are). The Internal Revenue Service does not require sole proprietors without employees to register. Owners can use their Social Security Number as the tax ID for their business. Here are some important points:

- Business expenses can be deducted. Contrary to common belief, it is not necessary to incorporate to be able to deduct your business expenses. A sole proprietorship that is not incorporated can still deduct business expenses.

- Profits are taxed by the proprietors. Proprietors are not allowed to pay themselves wages. The owners withdraw profits from the company as they need them. They owe income tax each year on all taxable business profits, whether or not they withdraw them.

- FICA and federal income taxes are applied to profits. FICA taxes (which pay for Social Security, Medicare, and other government programs) will be 15.3% up to $160,200 Social Security limits and 2.9% above that. Medicare taxes of 0.9% are also applied to self-employment incomes exceeding $200,000 in the case of single taxpayers. I have found that many sole proprietors who are small end up paying more FICA than federal income taxes, depending on their circumstances.

|

|

|

|---|---|

|

|

Cons |

|

Easy to install |

Profits subject to FICA tax |

|

Most owners can easily understand |

The owner’s assets will not be protected if the company isn’t formed as an LLC |

|

No need to file separate business tax returns |

|

|

There is no payroll to be run when there aren’t any employees |

|

What are partnerships?

The partnership is the multiple-owners version of sole proprietorship. In most states, forming and maintaining a partnership requires very little paperwork (if at all). It is because of this circumstance that many early stage businesses, which are relatively small and have not yet achieved significant profits, choose to be organized in partnerships rather than as formal corporations.

This arrangement is especially appealing for smaller companies with no employees in which owners perform the majority of work. Real estate holding companies and professional services firms such as accountants also use partnerships.

Although the paperwork for a multi-owner company is minimal, it’s more complex than a sole proprietorship. Therefore, a contract that governs the ownership and operations of the business, as well as the partnership, should be in place. You will also need to consider the following financial factors:

- The business income does not have to be distributed proportionally to the ownership. This is unique to partnerships. It is helpful to have this flexibility when there’s a silent investor who provides the majority of capital, but doesn’t expect a proportionate share in the profits. Such an arrangement should be detailed in the partnership agreement.

- The entire partnership’s taxable income, like that of sole proprietorships is subject to FICA taxes. It is for this reason that most large, profitable businesses are not partnerships. The tax burden becomes simply too great.

- The payments to partners do not constitute wages. The simplicity of partnerships is enhanced by the fact that partners are not paid wages but receive guaranteed payments in exchange for their service.

- If there aren’t any non-owners, the partnership does not need to file or run payroll. The partnership can avoid the hassle and cost of paying for payroll services. The savings may offset an increased FICA tax burden, depending on the size and scope of your company. This could make a partnership more attractive.

|

|

|

|---|---|

|

|

Cons |

|

Simple to install and use |

Profits subject to FICA Tax |

|

Most owners can easily understand |

The personal assets of the owners are not protected unless the company is structured as a Limited Partnership or LLC |

|

Flexible profit allocation allowed |

|

|

No payroll will run if no other employees than partners exist |

|

What are S Corporations?

Due to the way they are taxed, partnerships and proprietorships tend to become less attractive as companies grow more profitable. S-corporations are a great option for smaller and midsize private companies.

S-corporations and partnerships are both pass-through businesses, but the FICA tax is what makes them more attractive to larger companies. S corporations are required to pay their owners a wage that is reasonable (which will be subject to FICA taxes), however, the remainder of profits from business are only taxed on income.

Imagine a company that earns $1,000,000 per annum. Consider a business that makes $1,000,000 per year. Let’s assume the owner gets $100,000 in compensation and $900,000. The remaining $900,000. is profit. This chart shows that, if all other factors were equal, moving to S-corporation status could save you approximately $31,000 in FICA taxes per year.

|

|

||

|---|---|---|

|

|

|

|

|

Before owner compensation, taxable income |

$1,000,000 |

$1,000,000 |

|

Owners’ wages |

N/A |

$100,000 |

|

Guaranteed payments to owners |

$100,000 |

N/A |

|

Taxable business income remaining |

$900,000 |

$900,000 |

|

FICA Tax on Owner Wages |

$0 |

$15,300 |

|

FICA Tax on Owner’s Guaranteed Payments |

$15,300 |

$0 |

|

FICA Tax on the remaining income |

$31,346 |

$0 |

|

Taxes due to FICA |

$46,646 |

$15,300 |

Note: Calculations based on FICA thresholds for 2023.

This benefit may seem impressive, but it is not worth the cost for very small companies. Even a “solopreneur”, who has no employees, must file reports to the IRS and the state if necessary. This is a disadvantage to sole proprietorships and partnerships because of the added cost and administrative burden.

S-corporations are subjected to more stringent rules as well. You can, for example:

- In general, an S Corporation can only be owned by individuals US citizens and residents . There are some exceptions for trusts or estates.

-

Distributions of profits and dividends are to be allocated based on ownership.

- The use of losses can be restricted. An owner of an S-corporation that suffers losses in some circumstances may not be eligible to claim that loss as a deduction on his or her personal return. Losses would need to be carried over to the next year.

- The stock can be divided into voting shares and non-voting ones.

-

S-corporations can have up to 100 shareholders.

Legal requirements for setting up or maintaining S corporations often require an accountant and/or lawyer, increasing the costs. S corporations are popular despite these possible drawbacks. The FICA tax savings is hard to match, which accounts for their popularity. S corporations shield their owners assets in case of legal claims, something proprietorships or partnerships don’t do. By forming an S Corporation by electing to tax your LLC as you will be able to avoid many of the strict legal requirements.

Even after FICA tax, in some situations, a partnership may be more efficient tax wise than an S-corporation. This scenario involves the partners not paying themselves guaranteed payouts and treating all distributions as payments. This approach has some significant limitations. You should consult a tax professional to determine if this is the right choice for you.

|

|

|

|---|---|

|

|

Cons |

|

FICA Tax Exempts Earnings Above Wages |

Setup required for full legal set-up |

|

Legal shield for corporate functions |

Owners can find it difficult to understand |

|

Profit allocation rules and distribution policies that are rigid |

|

|

Limitation of deductions for losses |

|

|

Shares can only be owned by a single person. |

|

|

Stockholders are limited to 100 maximum |

|

|

The majority of the time, it must be owned and operated by an American citizen |

|

|

Even if you don’t have any non-owners, payroll must still be done. |

|

|

Stocks are limited to one type |

|

What are C Corporations?

The S corporation may become obsolete as businesses grow and get more complex. When the company has more than 100 shareholders (as in a publically held firm) or different share classes are needed, it is time to look at the C corporation.

The majority of large American corporations listed on the stock exchange are C-corporations. Rare are privately held C corporations, which typically use the structure to address other concerns than tax.

The C corporation is often used by high-growth companies seeking to raise series financing. Private companies that are seeking funding are often forced to use the C corporation structure because they are unable to obtain it through an S Corporation.

Delaware is the most popular state for US corporations. Its well-defined corporate laws and regulations, which have been tested in court, make it an ideal place to incorporate. Delaware claims that more than 68 percent of Fortune 500 firms are headquartered there.

The C-corporation structure has a significant disadvantage. As we discussed in the discussion on pass-through entities, the company is taxed on its income and the stockholders are taxed on their dividends.

In addition, losses incurred by C corporations cannot be offset against the personal income of stockholders. Many private companies are discouraged from using this type of structure because they face these problems.

The C-corporation structure is a good idea in certain situations. The cons of C corporations will outweigh their pros for most small and midsized businesses.

|

|

|

|---|---|

|

|

Cons |

|

Corporate profits taxed at a low rate |

Setup required for full legal set-up |

|

Legal shield for corporate functions |

Double Taxation on Corporate Profits |

|

Stockholders are allowed to hold unlimited amounts of shares |

Limitation of deductions for losses |

|

The term stockholder can include trusts, funds and other entities. |

|

|

Stocks can be sold tax-free upon exit |

|

After you’ve gotten a feel for the main characteristics of each of the business entities recognized as tax-deductible, we can examine whether forming an LLC is advisable for your firm.

What are Limited Liability Companies?

A limited liability company, as its name implies, is a type of business that provides “limited liability” for owners and tells everyone that they are not personally responsible.

The IRS does not recognize an LLC as a business entity that pays taxes. If the owner wants to set up the business as an LLC, they will also need to decide what type of company it is.

You can organize your business as one of the other four types that we have discussed, without having to be an LLC. The majority of new businesses are LLCs.

- An LLC protects an owner’s assets in the event of a business lawsuit. This would expose the business owner’s assets to possible claims.

- An LLC’s structure is easier to manage than traditional S and C corporations. While a corporation is taxed like a company, it is not required to keep meeting minutes or hold an annual meeting.

- An LLC can be converted to another entity later on, but the management and regulations of an LLC are easier. A common example is to first form an LLC that’s taxed like a partnership and then choose S corporation status once the business becomes profitable.

State governments are responsible for forming LLCs and other business entities. The exact procedure for forming a company will vary by state and could include different fees. State-specific corporate governance requirements and reporting obligations can also vary.

Federal tax laws do not change. Federal tax law is the same for all entities, no matter where they are registered.

Partnership, Proprietorship, C Corp, S Corp: In Review

The three most important factors to consider when selecting a company are the taxation of profits, administrative costs and complexity and liabilities.

Tax-wise, an S corporation is the best option, as it has a single taxing layer (unlike C Corporations) and its earnings aren’t subject to FICA taxes (unlike proprietorships and partnerships).

When you consider the costs and complexity involved in setting up and maintaining a sole proprietorship, it’s the best option. These are the easiest to set up and the least expensive. For a company with multiple owners, an LLC is often the best option. However, for more flexibility a partnership may be better.

The LLC structure offers the best protection against liability. The LLC structure offers protection from liability along with the other four structures. The liability protection offered by a non-LLC C or S corporation is also solid.

|

|

||||

|---|---|---|---|---|

|

|

|

|

|

|

|

Tax rate for profits in 2023 |

10%-37% |

10%-37% |

10%-37% |

21% |

|

Double taxation |

You can also find out more about the No. |

You can also find out more about the No. |

You can also find out more about the No. |

You can say that. |

|

FICA Tax on Profits |

You can say that. |

You can say that. |

You can also find out more about the No. |

You can also find out more about the No. |

|

Costs of setup/ongoing administration |

Low-cost |

Modest |

The High-quality |

The High-quality |

|

Protection from Liability |

You can also find out more about the No. |

No, in general |

You can say that. |

You can say that. |

|

Benefits of LLC umbrella |

Protection from Liability |

Protection from Liability |

Simpler governance |

Simpler governance |

What type of entity should you choose for your business?

In order to help you better understand how to choose an entity, I will use four fictional businesses to show how the different types of entities can benefit a company depending on its structure and the needs of the stakeholder.

1. The Summer Side Hustle

Joe’s Mowing

- Joe, a college student of 21 years old is looking to earn an additional income. He decided to open a small business in lawn care.

- Joe plans to buy equipment valued at $5,000, and hopes to make a profit for the summer of $15,000.

- Joe will be the only employee of Joe’s Mowing.

What Entity type is right for Joe’s Lawn Mowing?

Joe, a young businessman with a limited-term plan, is the perfect candidate to form a sole ownership. A S corporation, however, would be expensive to establish, and Joe would need to pay himself an appropriate wage (subjected to FICA taxes). The wage would wipe out the $15,000 profit and negate any FICA tax savings. The hassles of payroll administration would also be too much. If Joe wanted liability protection, an LLC umbrella could provide it.

2. The Apartments are Family Owned

LBD Group

- Lucia, Ben and Dorcas, siblings, own an equal percentage of a multi-unit apartment building.

- Lucia invests in the business, but she is not vocal about it. Ben and Dorcas are responsible for managing and maintaining the property.

- Lucia agreed to not receive a share of profits because her contribution to the project is only capital.

What Entity Type is Right for LBD Group

LBD Group would be better off with an LLC that is taxed like a partnership. The S corporation benefit isn’t applicable because rental income does not have to be subjected to FICA taxes. This group is interested in partnerships because they allow for unequal distribution of profits among owners. If the partnership were to exist, there would be no need for payroll because no employees other than owners are employed. An LLC offers protection for the owner in case of litigation, given that real estate businesses are prone to liability.

3. The Family Business of a Married Couple

Brilliant Ideas

- Bill and Malia founded a copywriting company called Brilliant Ideas.

- The company will end its first tax year with a $10,000 net loss, which includes only the six months following the founding of the business in June.

- The couple is confident that next year’s profits will reach $250,000.

What Entity Type is Right for Brilliant Ideas

Bill and Malia, who have a loss this year and a profit of $250,000 next year anticipated, are perfect candidates to . They can form an LLC, elect to tax as proprietorships or spouse partnerships this year and then choose S corporation status the following year. So they could use the losses from their business to offset income or wages. The S-corporation will pay them next year, but the profits remaining will be exempt from FICA.

4. Fintech startup run by several entrepreneurs

FreeBooks

- FreeBooks, a fintech company in its early stages led by a team of small entrepreneurs.

- Private equity investors are sought by the founders.

- It is the goal to enter the market in a year, and become a significant player within 3 years. This will require several capital injections.

What Entity Type is Right for FreeBooks

C corporations are the only option for a traditional technology start-up that wants to raise venture capital. Other types of entity would not allow for the complicated share classes and ownership structure that these companies need. It is possible to start as an LLC that’s taxed like a partnership, or as an S-corporation. Then switch over to C Corp status once corporate investors are a reality. This scenario would benefit from structuring your company as an L.L.C., as this would give you more flexibility in adjusting to these changes and keep the early stages simple. It would also allow investors to claim losses as a deduction on their tax returns.

Change your entity type to meet future needs

It’s exciting to start a company, but you also need to take care and do things correctly. Contact your tax advisor to get advice on the best entity for your situation.

It is difficult but possible to alter your business’s structure or entity later on as you see fit and your profitability changes. If you are starting a business that is more traditional (services, manufacturing, retail etc. ), for example, it’s possible to change the legal structure and entity type of your company later on as needs or profitability changes. Consider an LLC that is taxed like a partnership at first, and then switch to S Corporation status once it becomes relatively profitable. This gives you the flexibility and benefits of a limited partnership, but also avoids FICA taxes on your profits when revenue begins to flow. Remember that changing can result in tax consequences and a significant administrative burden.

Do your due diligence and weigh the pros, cons, and other factors of each option for your business. Your company will be on the right foot if you choose your entity correctly from the beginning.

The article was recently updated to include the most recent and accurate information. The comments below could predate the changes.